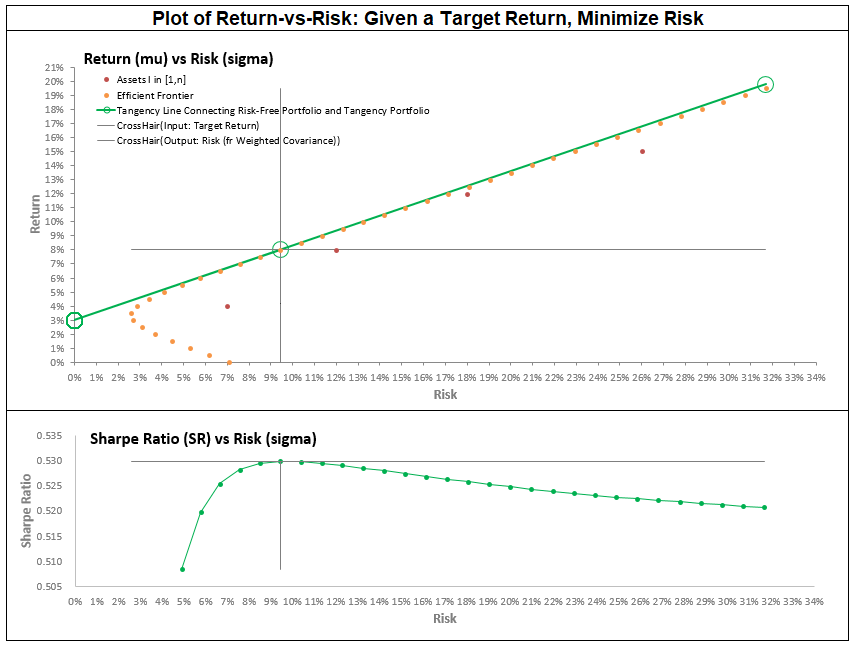

Portfolio Optimization for 20 Securities Using Lagrange Multipliers, No Short-Selling, Weights Sum to 1

Portfolio Optimization for 20 Securities Using Lagrange Multipliers, No Short-Selling, Weights Sum to 1

Problem:

Construct the Optimal Portfolio that:

delivers the target return (mu_Target)

with minimum risk

Minimize the risk of the portfolio (in this case, measured as half the variance)

While maintaining an expected return target of (mu_Target)

By adjusting the investment weights on each asset

Subject to the budget constraint that the weights sum to 1

Method:

Since constraints are equalities => We can use Method Lagrange

Supports up to 20 securities.

Able to do more if requested. Please contact us.

Constraints:

No short-selling (ie. No negative weights)

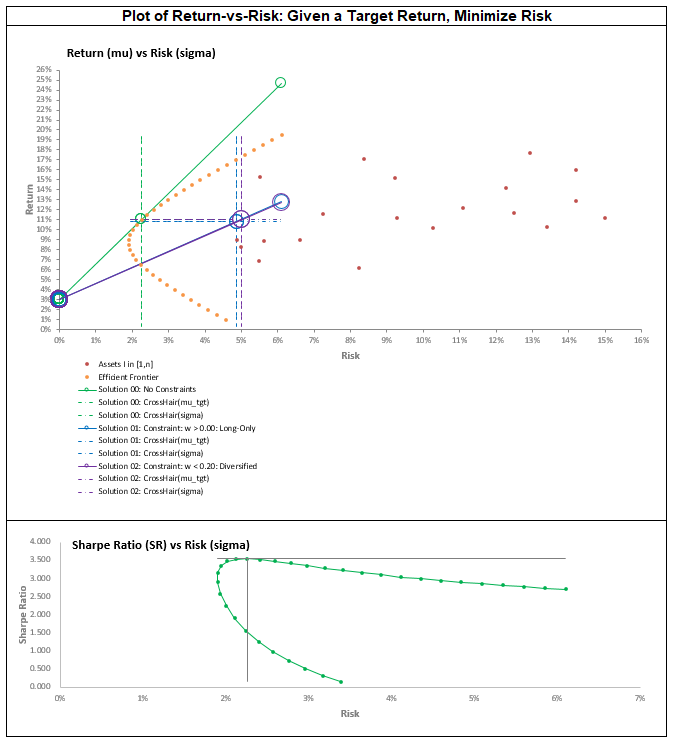

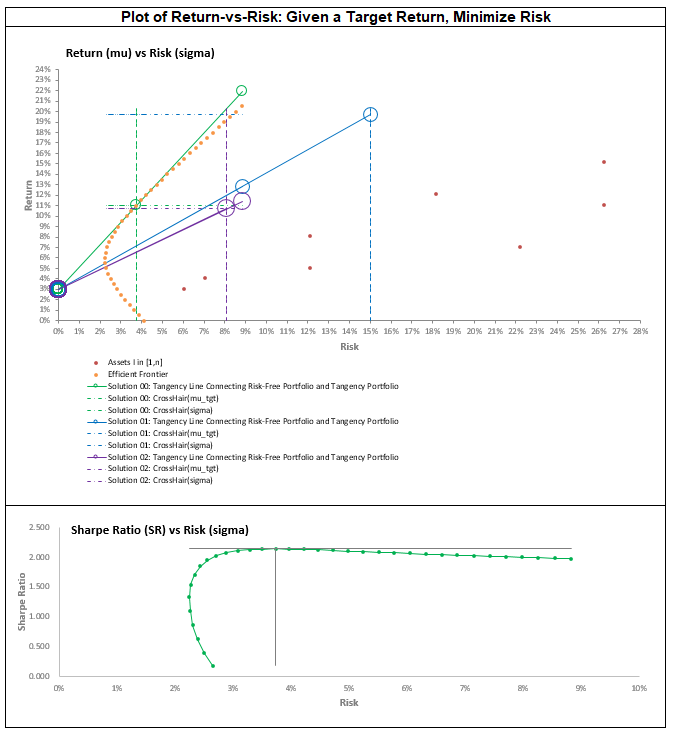

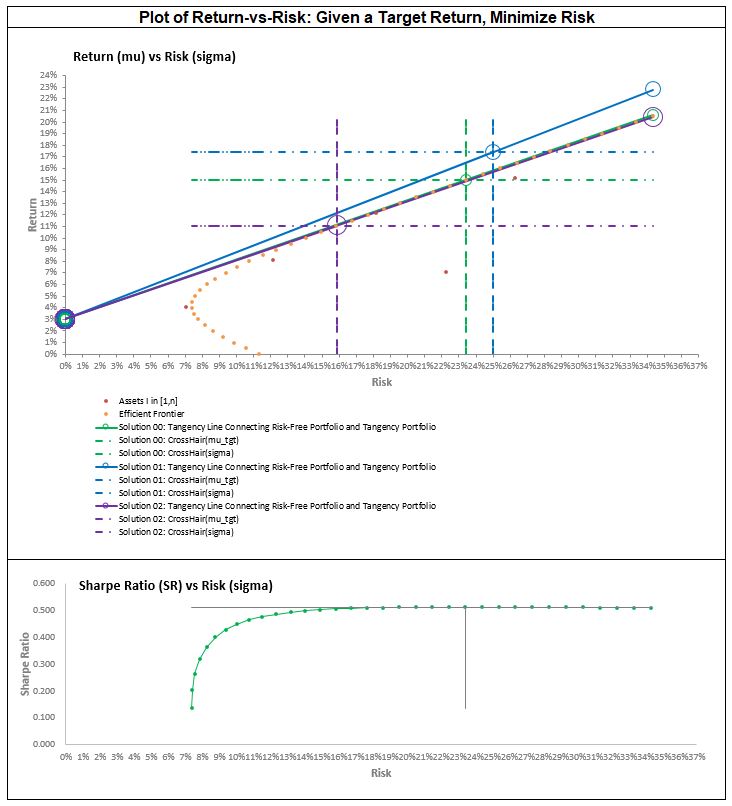

Solution 00:

Basic MPT with only budget constraint that weights sum to 1

Solution 01:

Tweaked solution where no negative weights are allowed,

but budget contraint fails, as sum of weights exceed 1.

Solution 02:

Maintain that no negative weights are allowed,

but normalize weights such that they sum to 1.

This yields a practical solution, but usually unable to meet target return.

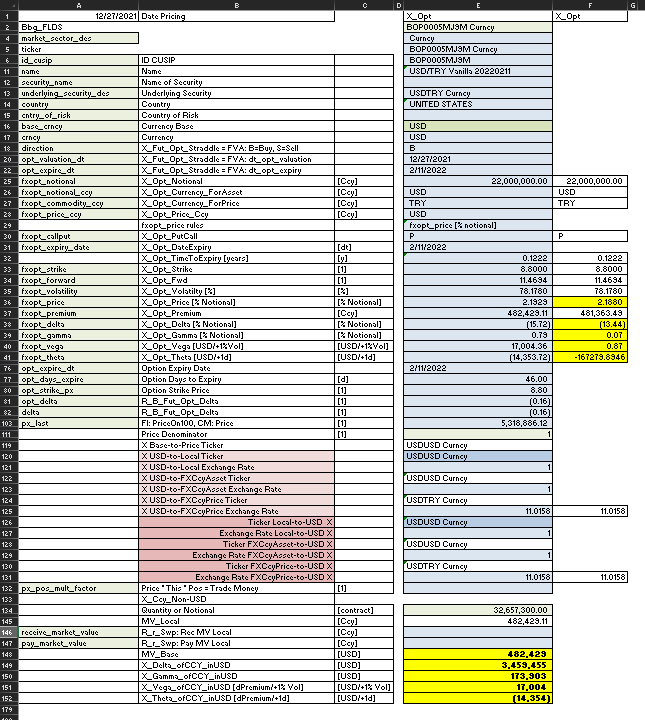

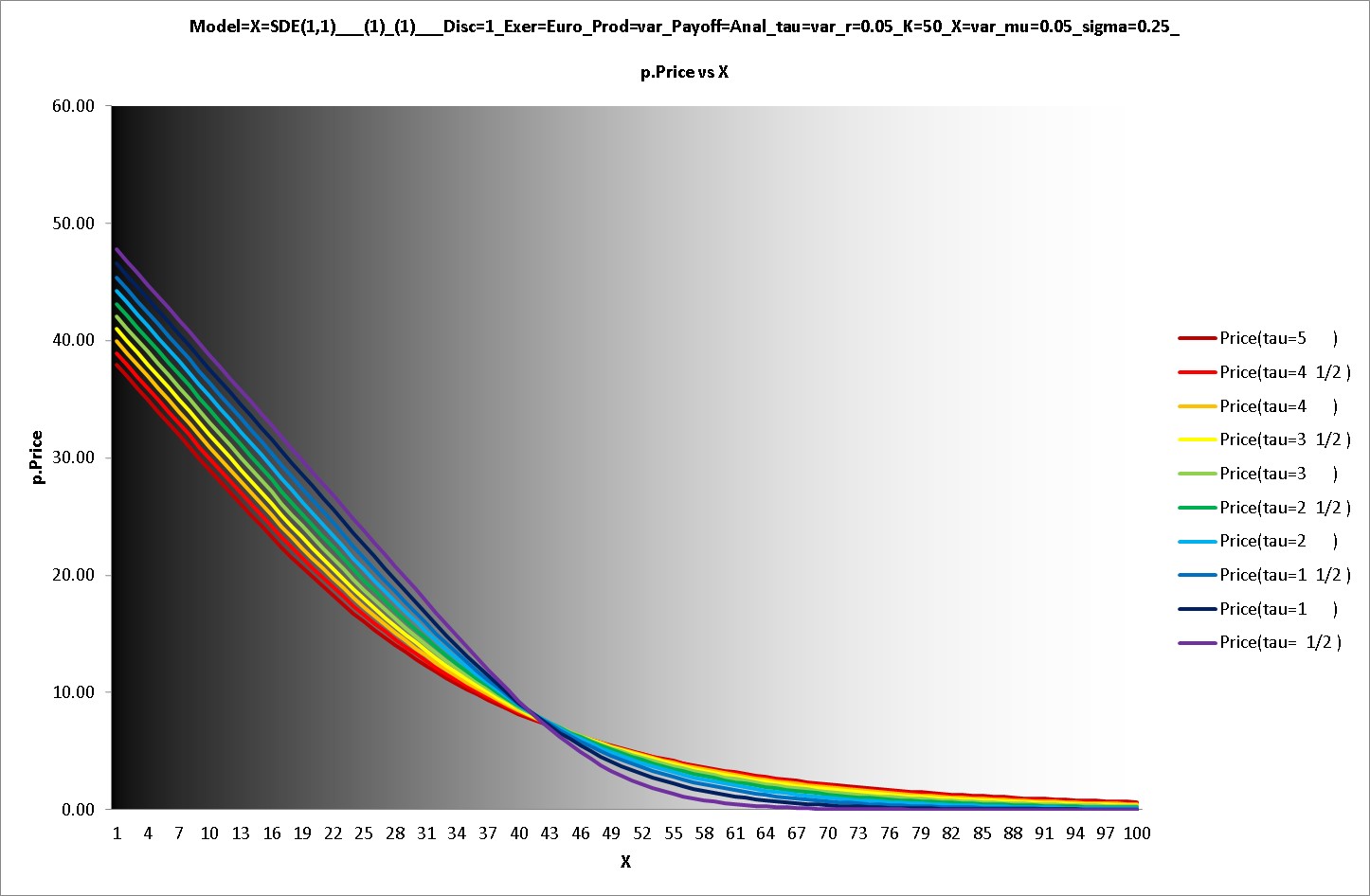

___(1)_(1)___Disc=1_Exer=Euro_Prod=var_Payoff=Anal_tau=var_r=0.05_K=50_X=var_mu=0.05_sigma=0.25_ChartSheet_01_p.Price")

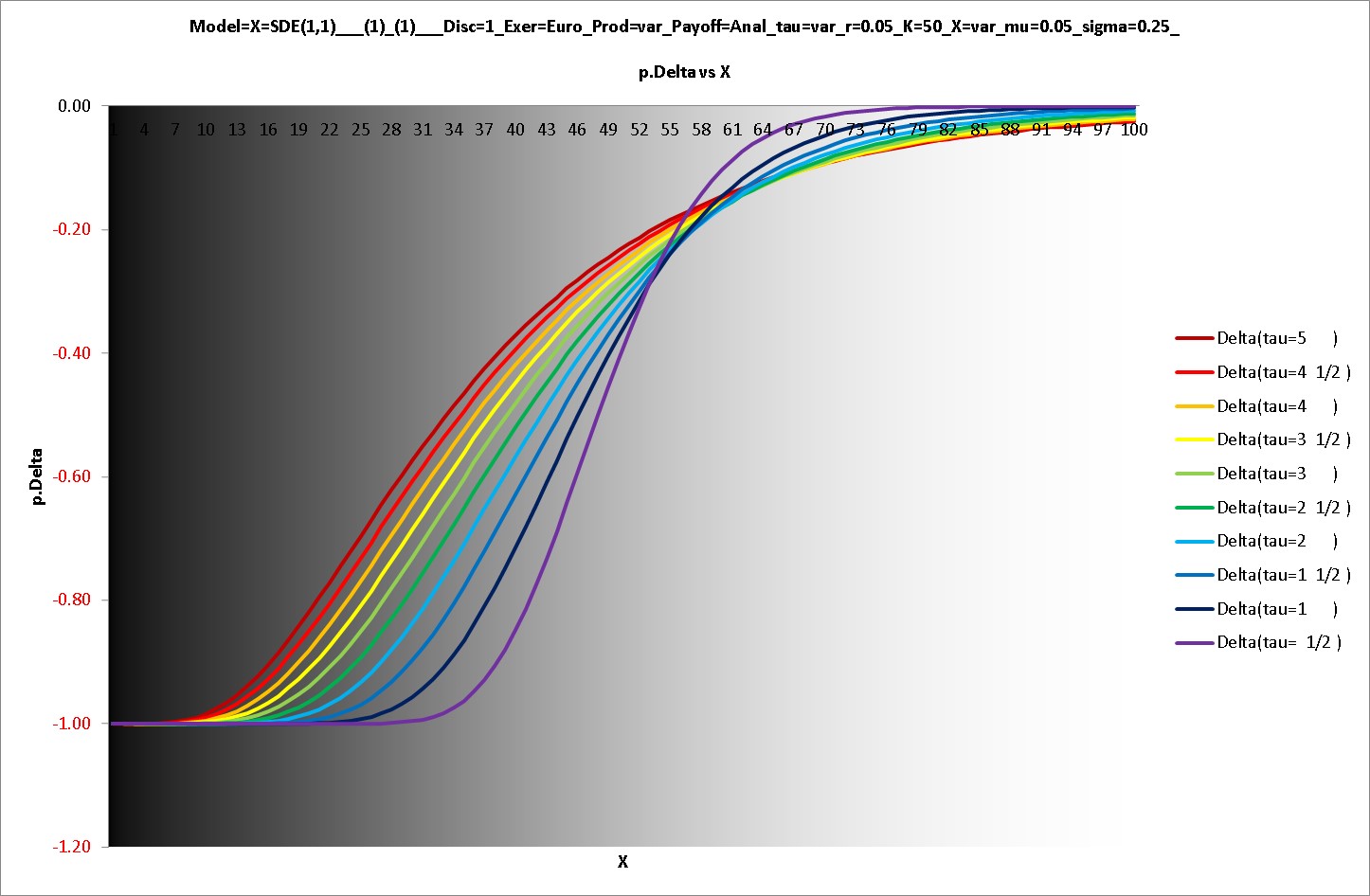

___(1)_(1)___Disc=1_Exer=Euro_Prod=var_Payoff=Anal_tau=var_r=0.05_K=50_X=var_mu=0.05_sigma=0.25_ChartSheet_02_p.Delta")

___(1)_(1)___Disc=1_Exer=Euro_Prod=var_Payoff=Anal_tau=var_r=0.05_K=50_X=var_mu=0.05_sigma=0.25_ChartSheet_03_p.Gamma")

___(1)_(1)___Disc=1_Exer=Euro_Prod=var_Payoff=Anal_tau=var_r=0.05_K=50_X=var_mu=0.05_sigma=0.25_ChartSheet_04_p.Speed")

___(1)_(1)___Disc=1_Exer=Euro_Prod=var_Payoff=Anal_tau=var_r=0.05_K=50_X=var_mu=0.05_sigma=0.25_ChartSheet_05_p.Vega")

___(1)_(1)___Disc=1_Exer=Euro_Prod=var_Payoff=Anal_tau=var_r=0.05_K=50_X=var_mu=0.05_sigma=0.25_ChartSheet_06_p.Volga")

___(1)_(1)___Disc=1_Exer=Euro_Prod=var_Payoff=Anal_tau=var_r=0.05_K=50_X=var_mu=0.05_sigma=0.25_ChartSheet_07_p.Vanna")

___(1)_(1)___Disc=1_Exer=Euro_Prod=var_Payoff=Anal_tau=var_r=0.05_K=50_X=var_mu=0.05_sigma=0.25_ChartSheet_08_p.Theta")

___(1)_(1)___Disc=1_Exer=Euro_Prod=var_Payoff=Anal_tau=var_r=0.05_K=50_X=var_mu=0.05_sigma=0.25_ChartSheet_09_p.ppmu")

___(1)_(1)___Disc=1_Exer=Euro_Prod=var_Payoff=Anal_tau=var_r=0.05_K=50_X=var_mu=0.05_sigma=0.25_ChartSheet_10_p.ppr")

___(1)_(1)___Disc=1_Exer=Euro_Prod=var_Payoff=Anal_tau=var_r=0.05_K=50_X=var_mu=0.05_sigma=0.25_ChartSheet_11_p.Rho")

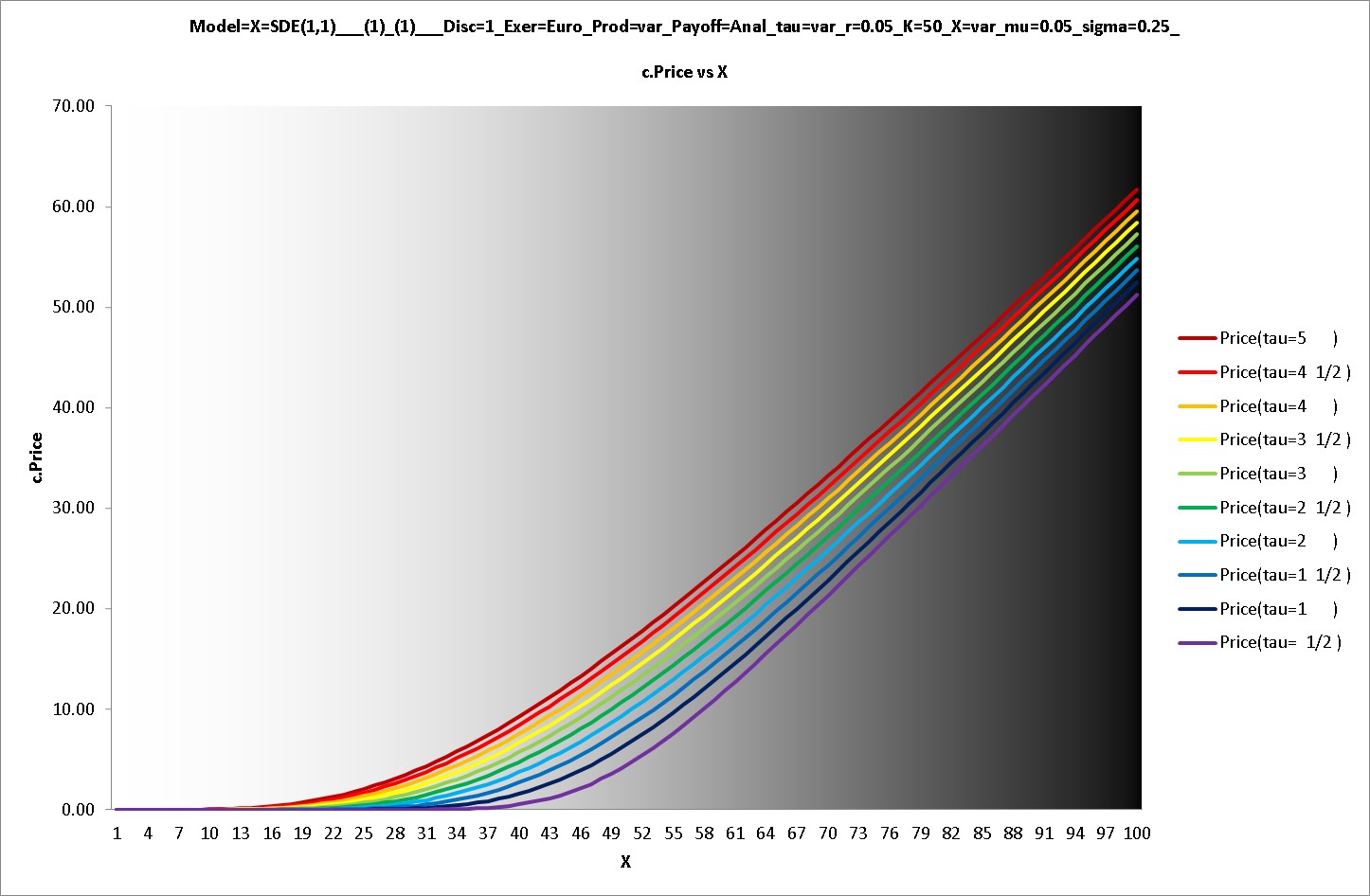

___(1)_(1)___Disc=1_Exer=Euro_Prod=var_Payoff=Anal_tau=var_r=0.05_K=50_X=var_mu=0.05_sigma=0.25_ChartSheet_12_c.Price")

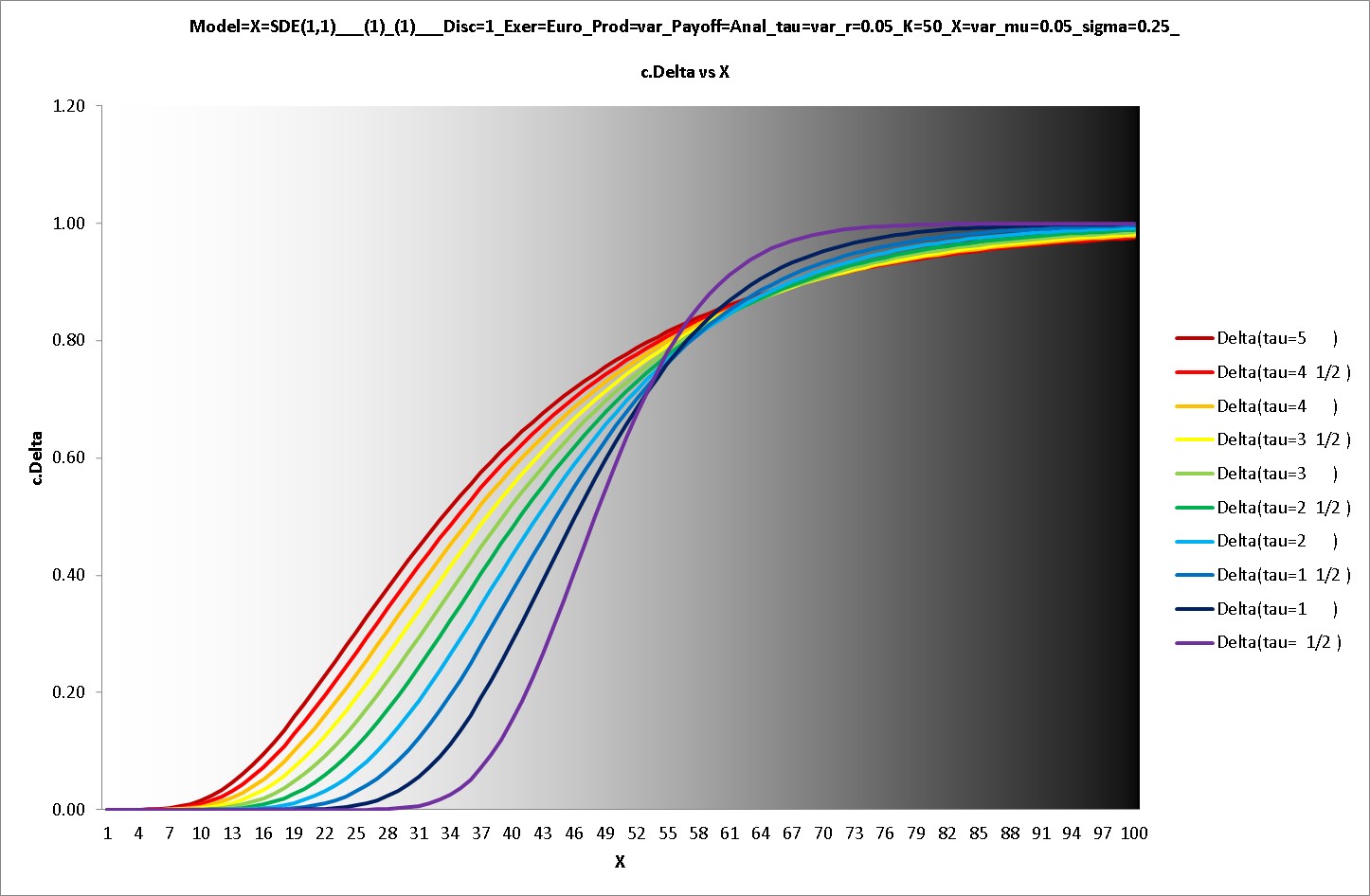

___(1)_(1)___Disc=1_Exer=Euro_Prod=var_Payoff=Anal_tau=var_r=0.05_K=50_X=var_mu=0.05_sigma=0.25_ChartSheet_13_c.Delta")

___(1)_(1)___Disc=1_Exer=Euro_Prod=var_Payoff=Anal_tau=var_r=0.05_K=50_X=var_mu=0.05_sigma=0.25_ChartSheet_14_c.Gamma")

___(1)_(1)___Disc=1_Exer=Euro_Prod=var_Payoff=Anal_tau=var_r=0.05_K=50_X=var_mu=0.05_sigma=0.25_ChartSheet_15_c.Speed")

___(1)_(1)___Disc=1_Exer=Euro_Prod=var_Payoff=Anal_tau=var_r=0.05_K=50_X=var_mu=0.05_sigma=0.25_ChartSheet_16_c.Vega")

___(1)_(1)___Disc=1_Exer=Euro_Prod=var_Payoff=Anal_tau=var_r=0.05_K=50_X=var_mu=0.05_sigma=0.25_ChartSheet_17_c.Volga")

___(1)_(1)___Disc=1_Exer=Euro_Prod=var_Payoff=Anal_tau=var_r=0.05_K=50_X=var_mu=0.05_sigma=0.25_ChartSheet_18_c.Vanna")

___(1)_(1)___Disc=1_Exer=Euro_Prod=var_Payoff=Anal_tau=var_r=0.05_K=50_X=var_mu=0.05_sigma=0.25_ChartSheet_19_c.Theta")

___(1)_(1)___Disc=1_Exer=Euro_Prod=var_Payoff=Anal_tau=var_r=0.05_K=50_X=var_mu=0.05_sigma=0.25_ChartSheet_20_c.ppmu")

___(1)_(1)___Disc=1_Exer=Euro_Prod=var_Payoff=Anal_tau=var_r=0.05_K=50_X=var_mu=0.05_sigma=0.25_ChartSheet_21_c.ppr")

___(1)_(1)___Disc=1_Exer=Euro_Prod=var_Payoff=Anal_tau=var_r=0.05_K=50_X=var_mu=0.05_sigma=0.25_ChartSheet_22_c.Rho")